In the context of privately held business entities, acquisitions generally proceed through either share purchase transactions, asset purchase transactions or statutory amalgamations. If acquisitions utilize shares or other securities of the acquiror as consideration, securities laws may apply, as well as additional tax considerations.

In a cross-border context, it is generally to the advantage of a foreign purchaser to use a Canadian acquisition vehicle when acquiring a Canadian target, which two companies are then often amalgamated post-closing. This structure is designed to ensure that the purchaser holds shares with high paid-up capital which can be distributed out on a tax-free basis (versus dividends, which would be subject to withholding tax). The amalgamation would also allow the expenses paid to finance the acquisition to be deducted from the target’s business income.

In cross-border transactions, “exchangeable share structures” are also often implemented when the purchaser wishes to use its own shares as consideration. Applicable Canadian tax law permits a deferral (or rollover) of capital gains tax only if the seller receives shares of a Canadian corporation. Where Canadian shareholders of the target may be subject to significant capital gains upon the sale, an exchangeable share structure may be preferable in order to defer their capital gains tax exposure until such time as such holders receive cash or liquid stock in order to fund such tax. In essence, the foreign purchaser incorporates a Canadian subsidiary that will issue shares that are exchangeable into the purchaser’s shares, where these exchangeable shares are the economic equivalent of the purchaser’s shares (for example through dividend entitlements and voting rights).

In the public company context, when the structures mentioned above are not available, acquisitions may also proceed by statutory plans of arrangement or take-over bids.

Share Purchase Agreements

Overview and General Utilization

Share purchase agreements involve a purchaser who buys all (or a majority) of the target company’s voting shares or ownership interest from the target company’s shareholders. This generally means that the ownership of the target company’s assets, rights, liabilities and obligations remains with the target. While the purchaser may receive the benefit of the target company’s assets and rights, it will also take on all of the liabilities and risks, including potentially those which are unknown at the time of the share purchase, unless the agreement requires those to be paid out by closing.

Advantages

A share purchase can be advantageous to a potential purchaser in the following ways:

From the perspective of the seller, a share purchase could offer the following benefits:

From a tax perspective, a seller of its shares in a Canadian company will derive tax advantages since the transaction will generally give rise to capital gains, which are effectively taxed at half the rate of ordinary income, any may be able to rely on a sizeable one-time exemption from capital gains tax if it is a Canadian resident and meets certain conditions. Additionally, if the consideration includes shares of a purchaser that is a Canadian corporation, the seller may be able to take advantage of tax deferrals or “rollovers”. A purchaser may wish to utilize a target’s non-capital tax-loss carry-forwards (i.e. business losses), which can only occur through purchasing the shares of the target.

Disadvantages

A share purchase can be disadvantageous to a potential purchaser in the following ways:

A share purchase can be disadvantageous to a seller in the following ways:

A share purchase will also generally result in a “change of control” of the target that triggers a year-end for tax purposes, requiring the target to file a tax return. Additional federal income tax rules apply to restrict the use of capital and non-capital losses upon a change of control, whereby, for example: (i) non-capital losses can only be used to offset future income from the same or similar business that generated them in the first place; and (ii) capital losses generally expire on a change of control. Accordingly, share purchases often involve a review of available tax elections to gross up the tax cost of capital assets of the target.

Main Documentary Requirements

Asset Purchase Agreements

Overview and General Utilization

In an asset purchase agreement, the purchaser will acquire specific assets and rights from the target seller and therefore assume responsibility for only certain liabilities. The parties to the transaction will negotiate which assets, rights and liabilities are purchased, keeping in mind that such assets, rights and liabilities must generally be able to function as a single unit to enable the target to keep running the business post-closing. The purchaser can therefore be selective in choosing which assets to buy and liabilities to assume. The seller will remain the legal owner of the company, if applicable, which may continue operating a separate business unit or be dissolved.

Some items that are commonly acquired in an asset purchase transaction include: business information, goodwill, information technology systems, IP rights, licences, personal and real property, and stock or inventory. Consideration will also be given to which employees are offered employment by the purchaser, who will be responsible for any severance liabilities, and how employee benefit plans are transferred/assumed.

Certain liabilities will nevertheless follow the assets to the new owner and, by operation of law, cannot be contracted out of. Most typically, these include environmental liabilities associated with real property, or collective agreements relating to unionized employees.

Advantages

An asset purchase can be advantageous to a potential purchaser in the following ways:

An asset purchase can be advantageous to a potential seller in the following ways:

An asset purchase is generally more advantageous to the purchaser from a tax perspective, because it receives the full cost base in the acquired assets which normally increases available deductions for depreciable assets and reduces gains on the subsequent sale of the assets. For non-resident purchasers, additional considerations will apply when structuring the transaction, for example in moving assets to/from Canadian versus foreign affiliates. In a share purchase, it may not be possible for a non-resident buyer to move assets out of the Canadian company post-closing without triggering Canadian tax.

From the seller’s perspective, an asset purchase may be preferable to enable the target seller to generate income or capital gains from the sale of assets that can be sheltered by utilizing any significant tax-loss carry-forwards it may have accumulated.

Disadvantages

An asset purchase can be disadvantageous to a potential purchaser in the following ways:

An asset purchase can be disadvantageous to a potential seller in the following ways:

Main Documentary Requirements

Asset purchases also involve allocating the purchase price among the various assets being sold, which is important from an income tax perspective given the deductibility of various types of assets.

General Timeline

*Since the duration of share and asset purchase transactions can greatly vary depending on the circumstances and size of the deal, only a general process has been provided below. The parties and their legal advisors will also have to consider what third party consents, if any, would be required, as often certain regulatory licenses and permits, and certain contracts, including loan agreements, may contain restrictions on changes of control.

Amalgamations

Overview and General Utilization

While amalgamations are often stated to be the Canadian equivalent of a merger in the United States, it is important to note that there are key differences between the two concepts. Amalgamations are a means of combining two or more incorporated businesses, known as the predecessor corporations, into one overarching business, known as the successor corporation or Amalco. In Canada, when the predecessor corporations combine, neither is formally dissolved. Rather, they simply continue to exist as one amalgamated corporation which shares each predecessor corporation’s assets, rights, liabilities and histories.

Amalgamations in Canada can take two forms, one being a long-form amalgamation (which occurs between arms-length companies and will require a shareholder vote) and the other being a short-form amalgamation (which occurs between related companies and can usually be approved through directors’ resolutions). One unique consideration is that since amalgamations in Canada are governed by statute, the predecessor corporations must be incorporated under the same statute, meaning that if one predecessor corporation is incorporated provincially while the other predecessor corporation is incorporated federally, then one of the corporations must file a certificate of continuance under the other’s statute. While amalgamations are not unheard of in the private context, typically when a target company has a large number of shareholders making it impractical to proceed by way of share purchase agreement, they are much more commonly used in the public context.

Three-Cornered Amalgamations

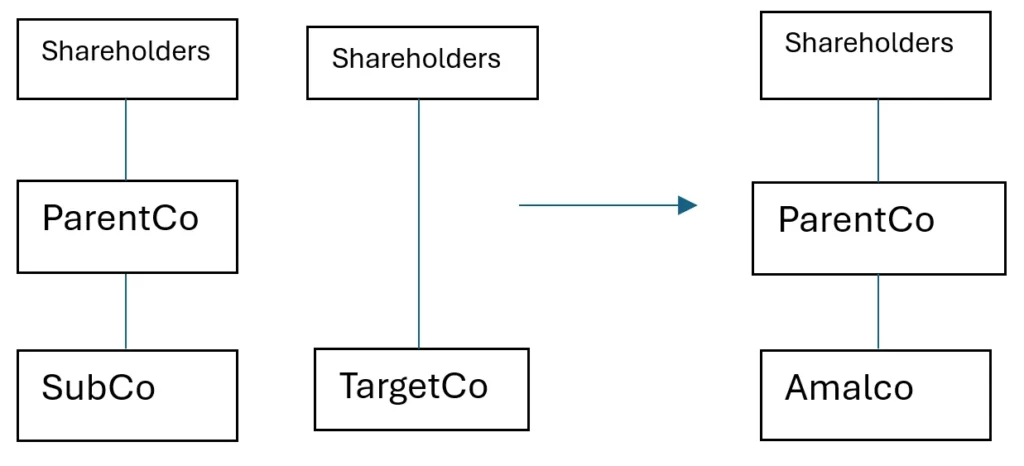

A triangular or three-cornered amalgamation can be used to effect an acquisition using consideration comprised of shares, or a combination of cash and shares. It is frequently utilized as an alternative to the takeover bid process under securities laws. For example, if a Canadian public corporation (ParentCo) wants to acquire the shares of another Canadian corporation (TargetCo) for share consideration, the transaction could be structured as: (i) a share-for-share takeover bid, (ii) a standard amalgamation of ParentCo and TargetCo, or as a triangular amalgamation of a subsidiary of ParentCo (SubCo) and TargetCo where TargetCo shareholders receive shares of ParentCo instead of shares of the amalgamated corporation (Amalco). In this case, ParentCo controls Amalco immediately following the amalgamation.

Using an amalgamation in the takeover context allows for the ability to implement the transaction with a two-thirds approval threshold of the votes cast at a shareholders’ meeting. Under a formal takeover bid, the acquiror would have to rely initially on tenders to the offer, and meet the thresholds of tenders to implement the compulsory squeeze-out provisions of corporate law to acquire any non-tendered shares, as discussed below.

Compared with a standard amalgamation, which requires the approval of shareholders of both ParentCo and TargetCo, a three-cornered amalgamation will not ordinarily require the approval of ParentCo shareholders, unless stock exchange policies so require it. This structure would also normally allow selling shareholders to obtain tax-deferred rollover treatment, if certain conditions under applicable tax law are met.

Advantages

The most notable advantage of amalgamations is that they are generally considered to be tax neutral. Section 87 of the Income Tax Act (Canada) states that amalgamating businesses can transfer tax attributes such as tax credits and capital losses to the successor corporation, thereby maintaining any tax advantages already existing. Further, since the assets of the predecessor corporations naturally flow to the successor corporation, rather than through a formal acquisition or purchase of assets, no immediate tax liability nor transfer taxes are triggered.

Disadvantages

The disadvantages of amalgamations are usually context specific. For example, if two major public corporations who are in the same industry amalgamate, then there may be a risk of forming a monopoly, which may triggers anti-trust legislation. Further, the successor corporation will maintain all liabilities, debts and obligations of the predecessor corporations even after amalgamation.

Amalgamations requiring shareholder approval may also operate on a lengthier timeline if a large number of shareholders need to be canvassed in order to obtain the necessary support. Each applicable corporate statute provides the necessary shareholder approval threshold for completing an amalgamation, which is at least over 50%, which threshold may increase given the provisions of applicable shareholder agreements or rights attributed to other share classes, such as preferred shares. Support agreements are often utilized in order to ensure the parties that the requisite shareholder approval will be satisfied. Timing may typically proceed faster in a private company context, as the corporate charter documents normally allow for a compressed notice period for a shareholders’ meeting, whereas in the public company context additional securities laws apply given the search processes involved in order to determine who the shareholders who are entitled to vote are as of a given record date.

General Timeline

The timeline below assumes a longer notice period prior to a meeting of the shareholders.

Main Documentary Requirements

Usefulness of Valuations and Opinions

Whether a valuation is required will depend on the specific circumstances of the amalgamation. Where not required by law, valuations may be useful to validate the consideration offered and mitigate the risk of shareholder exercising their rights of dissent. If one is required (for example in related party transactions), it must be obtained before sending the proxy circular to shareholders and it must be sent along with the proxy circular. The directors of the target company may also choose to obtain a fairness opinion from their independent financial advisors inquiring into what is the appropriate consideration for its shareholders under the amalgamation.

Plans of Arrangement

Overview and General utilization

A plan of arrangement is a flexible structuring tool commonly used in Canadian mergers and acquisitions, particularly in the public company context. It is a court-supervised statutory process that gives companies the ability to accomplish a variety of “fundamental changes” such as a reorganization, a merger with another company, or an exchange of assets, all in a single step under the procedures found in the Canada Business Corporations Act or its equivalent provincial legislations. The reasoning behind choosing a plan of arrangement generally involves a need to make significant changes to corporate structure in order to maintain fairness to the shareholders whose rights may be affected in a complex merger. Once a definitive agreement is reached between the bidder and the target company, the plan of arrangement will require both majority shareholder approval (typically approval by holders of 66 2/3% of the outstanding shares) and court approval before being effectuated. The court approval process ensures the transaction is binding on all securityholders, even dissenters and, in some instances, creditors, where the court order approving the arrangement confirms the plan is fair and reasonable to all parties involved.

While more commonly used for public companies, plans of arrangement are being increasingly utilized in the private sphere for companies which have a large number of shareholders.

Advantages

Plans of arrangement can deal with multiple aspects of a deal, such as tax planning or addressing multiple classes of securities, all in one step, making it a more efficient process. Additionally, arrangements provide the greatest amount of flexibility to the parties involved, especially if certain securityholders of the target will need to be be compromised or otherwise have their rights modified, and can be customized to address the specific goals at hand. If applicable, there are some advantages to U.S. acquirors who obtain securities pursuant to plans of arrangement as they will be exempt from registering their securities with the SEC due to plans of arrangement being considered corporate-level transactions instead of formal tender offers under U.S. securities laws.

Disadvantages

Given that there is a level of judicial discretion involved as court approval is required, parties must prepare their materials with a view to satisfying the court that the arrangement serves a valid business purpose, is fair and reasonable to securityholders and responds adequately to those whose rights are being affected. As a result, the use of fairness opinions or valuations become more relevant as tools to validate the offer. This court process also gives unsatisfied securityholders a platform to voice their objections, which can cause delay or the ultimate failure of the transaction. Further, the need for both shareholder and court approval means that plans of arrangement can require longer timelines to complete, especially as these transactions will need more fulsome disclosures to be prepared. Those on the acquiror/bidder side should keep in mind that plans of arrangement are a target-driven process and thus, the acquiror will have limited control over the timing and preparation of documents (compared to, for example, a take-over bid made by the acquiror directly to the target’s shareholders).

General timeline

Main Documentary Requirements

Usefulness of Valuations and Opinions

While not a set requirement, courts generally have an expectation that a valuation and a fairness opinion from the target’s independent advisors will be included in the materials submitted to court in asking for their approval. Such documents, if applicable, will be sent to shareholders along with the proxy circular.

Take-over Bid

Overview and General Utilization

A take-over bid will be triggered when an offer is made from an acquiror directly to the shareholders of the target to acquire voting or equity securities of a class where the securities implicated (in addition to any securities already beneficially owned by the acquiror and its affiliates, if any) will constitute 20% or more of all outstanding securities of the class. In measuring what constitutes 20% ownership, acquirors must include all securities that it beneficially owns or has control over as well as any securities that the acquiror has a right to acquire within 60 days, such as options.

Once the 20% threshold is reached, take-over bid rules will be triggered such as mandating the acquiror to make the same offer to all of the target’s shareholders with identical consideration and no collateral side agreements, absent any exemptions. Other rules that will be triggered include the mandatory bid period timeline where the bid must be open for 105 days, which may be shortened to a minimum of 35 days at the discretion of the target, as well as the minimum tender condition whereby more than 50% of securities owned by persons other than the acquiror must be tendered to the bid before the acquiror may take up any securities under the bid.

Take-over bids are typically used to acquire public companies and can take either a friendly or hostile form, as will be discussed below. This type of transaction is often considered the Canadian equivalent to a U.S. tender offer. Take-over bids technically also apply to offers made for the shares of a private company, but most acquirors in this context would be able to avail themselves of applicable exemptions to the formal bid requirements under Canadian securities law. Take-over bids may also be a preferred option in the context of private company acquisitions where there is a large shareholder base and valuations may be complicated or prohibitively expensive. In the private company context, the acquiror would seek exemptive relief from securities regulators to avoid the application of the formal take-over bid rules, in particular if it intends to use its own shares as consideration.

Advantages

This process is the only one available for unsolicited or “hostile” bids, meaning that the agreement of the target itself is not required and the acquiror can force an acquisition through negotiations with the shareholders of the target.

Despite the 105-day minimum offer period, take-over bids can potentially be completed much faster, particularly if the transaction is friendly, as the target board may waive the minimum period to as short as 35 days.

For the acquiror, a take-over bid can give them more control compared to other forms of acquisitions given that the acquiror is the one who determines the initial bid price and the timing of the launching of the transaction.

Disadvantages

A second-step transaction may be required to gain 100% ownership of the target if the acquiror is unable to obtain at least 90% of the target’s securities in the initial bid.

If the take-over is hostile, then the transaction may take significantly longer to complete than other acquisition transactions.

A hostile target board can recommend to their shareholders to reject the take-over bid and in general, utilize a variety of defence tactics to make the entire transaction a more difficult process (for example, in providing access to due diligence documents).

General timeline

Hostile

Friendly

Main Documentary Requirements

In the public company context, a bid whereby the acquiror offers its own shares as consideration will be subject to prospectus-level disclosure in its offering documents, which makes the preparation of the circular a more complex process.

Valuation

The acquiror may be required to include a valuation of the public company target performed by an independent party in its disclosure materials.

{kind=link}

{kind=link}